Thinking about refinancing your mortgage? One of the first questions you probably have is: “Do I need to prove my income to qualify?” Understanding the refinance income requirement check can feel confusing, but it’s a crucial step to ensure you get the best deal possible.

Whether you’re employed, self-employed, or have a unique income situation, knowing what lenders look for can save you time and headaches. You’ll discover exactly what income documentation is needed, how lenders evaluate your earnings, and tips to improve your chances of approval.

Keep reading to unlock the secrets that can help you confidently navigate the refinancing process and potentially lower your monthly payments.

Income Verification Basics

Income verification is essential when refinancing a mortgage. It shows lenders you can repay the loan. Lenders want to see stable and reliable income. This helps reduce their risk of lending.

Common documents include pay stubs, tax returns, W-2 forms, and bank statements. These prove how much money you earn and where it comes from. Self-employed borrowers may need to provide profit and loss statements.

Employment stability is another key factor. Lenders prefer borrowers with steady jobs. This means no frequent job changes or gaps in work history. A stable job signals steady income and repayment ability.

Income Requirements By Loan Type

Conventional loans require proof of stable income and good credit history. Lenders want to see that borrowers can handle monthly payments. Employment verification and pay stubs are common documents needed.

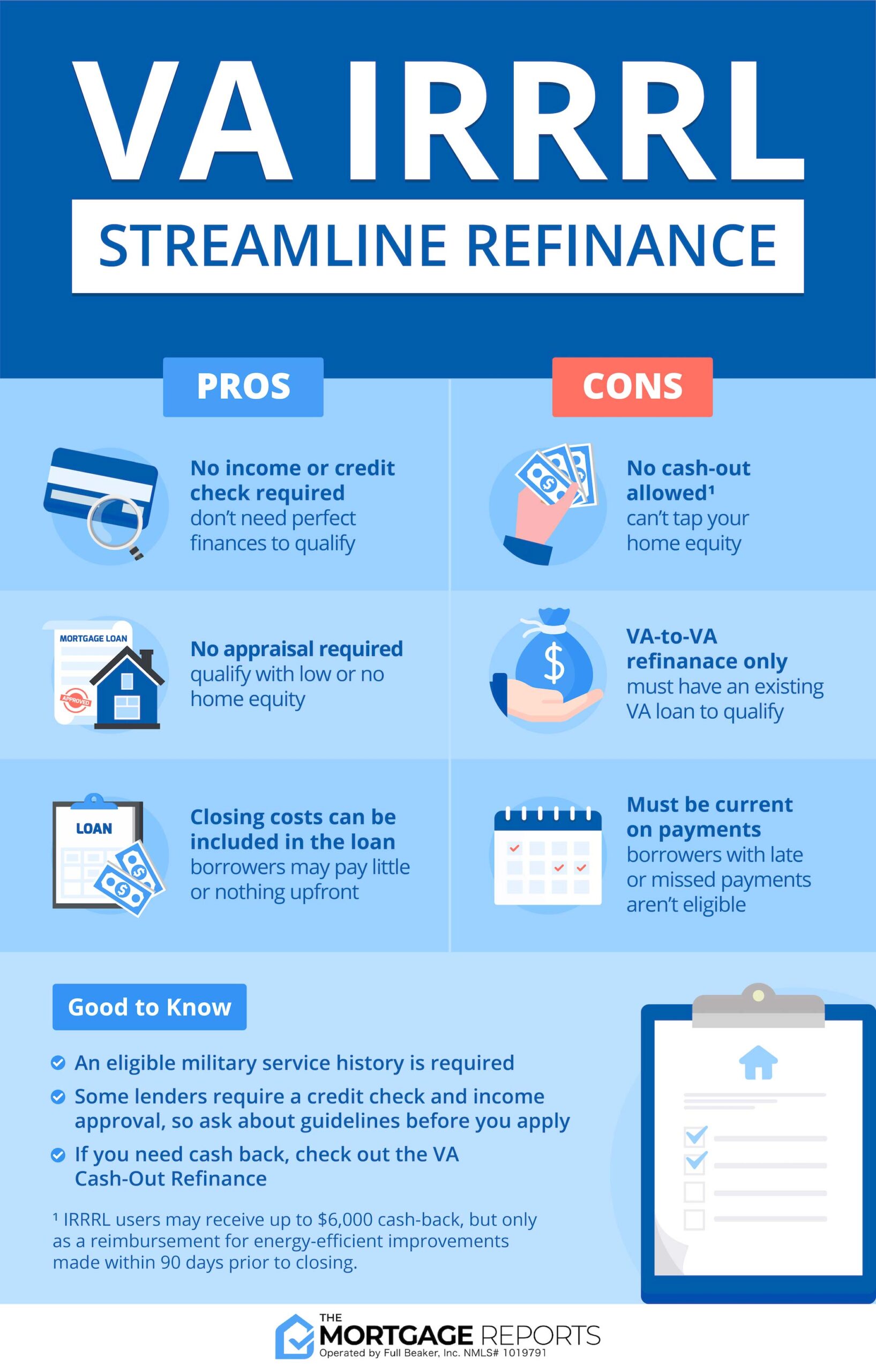

FHA Streamline Refinance often skips income verification and appraisal. This option suits borrowers with existing FHA loans. It helps lower payments without showing current income or job status.

Non-QM loan options serve borrowers with unusual income sources. These loans accept alternative proofs like bank statements or rental income. They are flexible but may have higher interest rates.

Special Considerations For Self-employed Borrowers

Self-employed borrowers often face unique income verification challenges. Bank statement verification is a common method lenders use. They review deposits over the past 12 to 24 months. This helps confirm consistent cash flow and business stability.

Alternative income proof might include profit and loss statements, tax returns, or 1099 forms. These documents offer a broader view of income beyond pay stubs.

Challenges include fluctuating income and irregular deposits. Lenders may ask for additional paperwork or longer documentation periods. Solutions involve keeping detailed financial records and working with lenders experienced in self-employed loans.

Impact Of Low Or Variable Income

Qualifying with low income can be challenging but not impossible. Lenders often look for stable income to approve refinancing. Showing consistent payments and job history helps.

Using home equity can improve chances. It acts as extra security for the lender. The more equity you have, the better the terms might be.

| Loan Program | Features | Best For |

|---|---|---|

| FHA Streamline | No income verification in many cases | Borrowers with low or variable income |

| Non-QM Loans | Flexible income requirements | Self-employed or irregular income earners |

| Government Programs | Lower credit score and income limits | Low income and first-time refinance borrowers |

Common Disqualifiers In Income Checks

Unstable employment often causes refinancing denial. Lenders want to see a steady job history. Frequent job changes or gaps can raise doubts about your income reliability. This makes it hard to prove you can pay back the loan.

Insufficient income is another common issue. Your earnings must cover the new monthly payments comfortably. If your income is too low, lenders may reject your application. They check if you have enough money for bills and other expenses.

Credit issues related to income include late payments or high debt. These problems suggest financial strain. Lenders worry you may struggle to make timely payments. Poor credit records linked to income can stop refinancing approval.

Steps To Prepare For Income Verification

Gathering required documents helps prove your income for refinancing. Common papers include pay stubs, tax returns, bank statements, and W-2 forms. Lenders need these to confirm your earnings. Organize them neatly to speed up the process.

Improving income stability means showing steady earnings over time. Avoid job changes before refinancing. Consistent income reassures lenders about your ability to pay. You might also explain any gaps in work history clearly.

Working with your lender involves clear communication. Ask what income proof is needed. Share all documents quickly to avoid delays. Your lender guides you through the steps. Trust and honesty help ensure smooth refinancing.

Frequently Asked Questions

Does Refinancing Require Income Verification?

Refinancing usually requires income verification to prove stable employment and ability to pay. Some programs, like FHA Streamline, may waive this.

How Much Of A House Can I Afford If I Make $70,000 A Year?

With a $70,000 annual income, you can typically afford a home priced around $280,000 to $350,000. This varies by debt, credit, and down payment.

What Disqualifies You From Refinancing?

Poor credit score, unstable income, high debt-to-income ratio, insufficient home equity, or recent bankruptcy can disqualify you from refinancing.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your new monthly mortgage payment should be at least 2% lower than your current payment. This helps ensure refinancing saves you enough money to justify closing costs.

Conclusion

Refinancing usually needs proof of steady income. Lenders want to see you can pay your loan. Different programs have different income rules. Some loans help those with lower or irregular income. Knowing your income situation helps you prepare better. Always check specific lender requirements before applying.

This makes refinancing smoother and less stressful. Keep your documents ready for quick verification. Smart planning leads to better refinance outcomes.

Read More

- Refi Credit Qualification Guide: Unlock Expert Tips for Approval

- Installment Loan Refinance Options: Smart Ways to Save Big Today

- Fast Refinance Approval Process: Unlock Quick Cash with Ease

- Personal Loan Refinance Quote: Unlock Lower Rates Today!

- Consolidation Refinance Quote: Unlock Savings with Smart Rates

- Refinance Quote Comparison Online: Save Big with Smart Choices

- Student Loan Refi Estimate: Unlock Savings with Smart Strategies

- Instant Refi Quote Estimate: Unlock Savings with Fast Rates

- Refi Pre Approval Online: Fast, Easy, and Stress-Free Guide

- Jumbo Refi Quote Comparison: Save Big with Top Rates Today